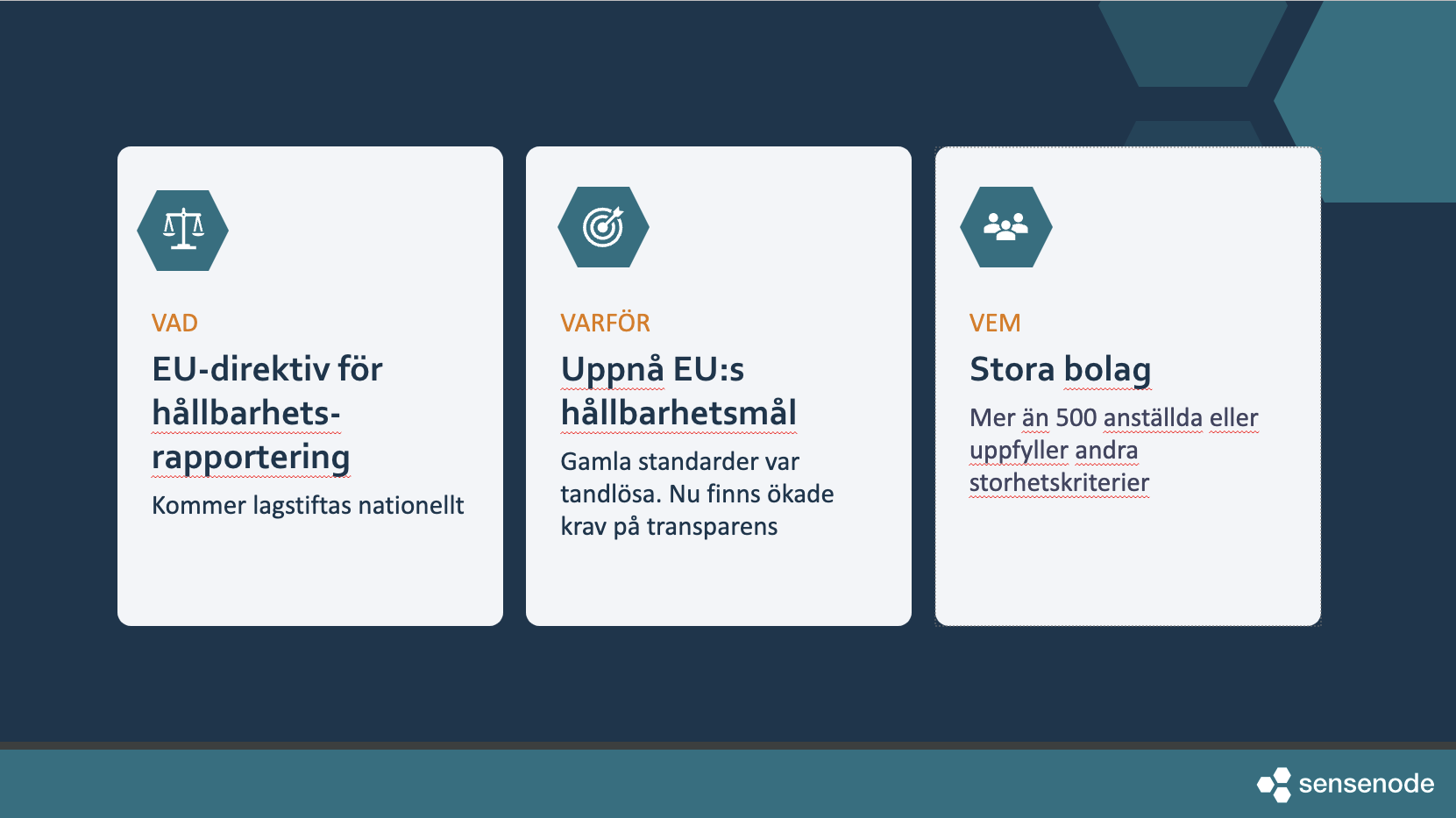

ENKLARE OCH BÄTTRE RAPPORTERING

CSRD-direktivet

CSRD (Corporate Sustainability Reporting Directive) är ett EU-direktiv som syftar till att förbättra företags hållbarhetsrapportering. Direktivet är en del av EU:s breda initiativ för att uppnå sina hållbarhetsmål. Genom ökad transparens gör CSRD det tydligare vilka företag som seriöst engagerar sig i hållbarhetsfrågor.

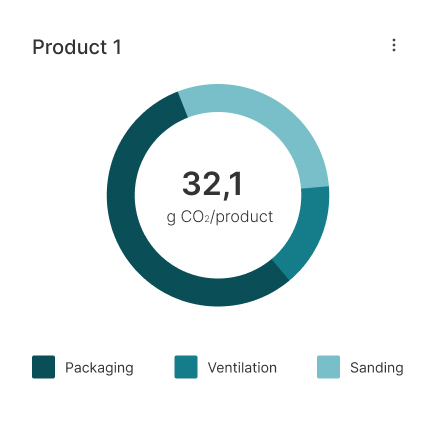

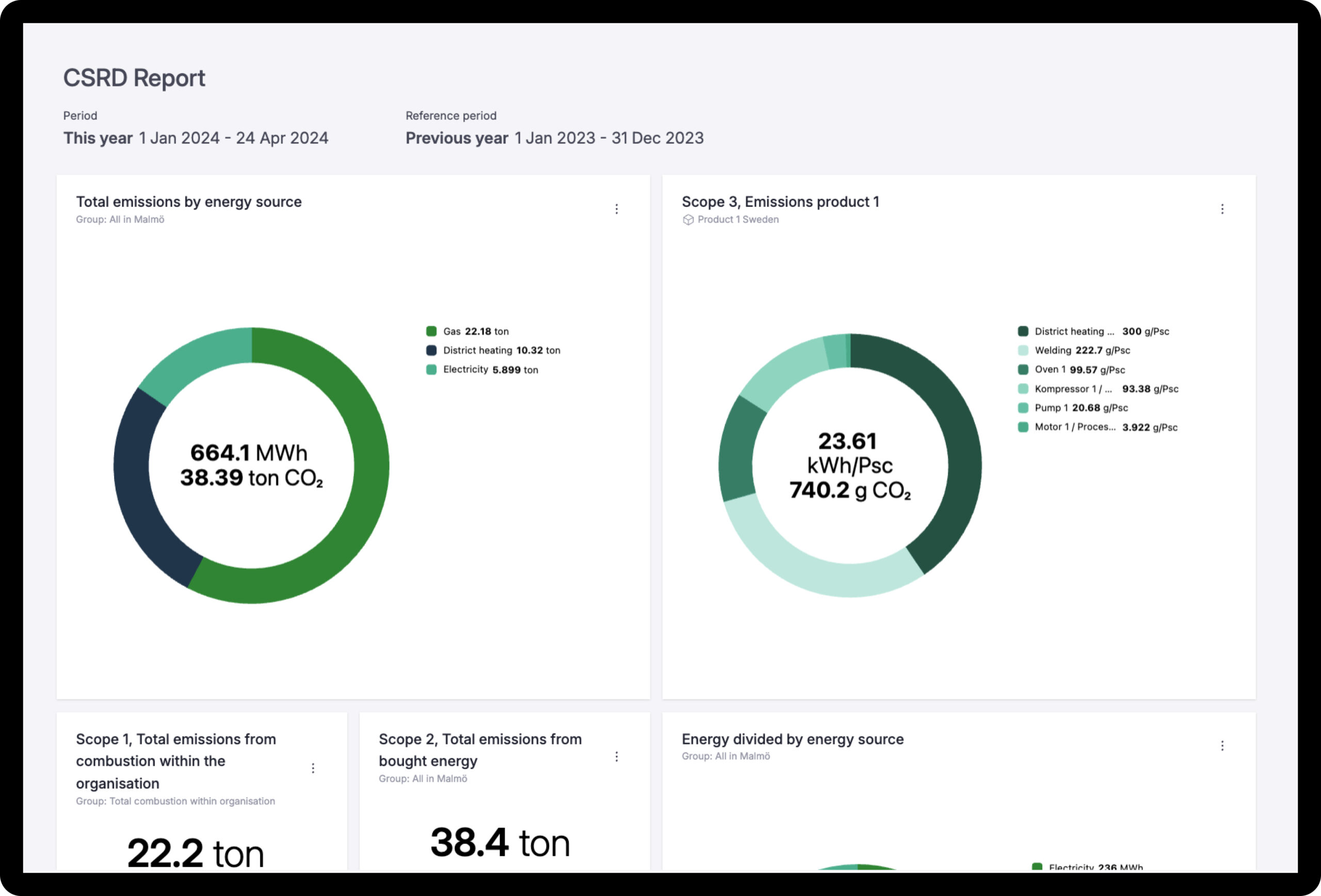

Att kontinuerligt mäta och genomföra hållbarhetsinsatser ger inte bara en konkurrensfördel. Det förstärker även företagets synlighet i hållbarhetsrapporter, särskilt gällande Scope 3-utsläpp.

- Automatiskt

- Transparent

- CO₂/enhet